Welcome to  -

Marg ERP 9+

-

Marg ERP 9+

Home > Margerp > Tax Clubbing > How to view Tax clubbing Report in Marg Software ?

How to view Tax clubbing Report in Marg Software ?

Overview of Tax Clubbing in Marg Software

Process of Tax Clubbing in Marg Software

OVERVIEW OF TAX CLUBBING IN MARG SOFTWARE

- Tax Clubbing means clubbing both input and output tax of a particular month and then a journal entry is being passed at the end of the month which is required for GST Payable.

PROCESS OF TAX CLUBBING IN MARG SOFTWARE

- Go to GST > Tax Clubbing.

A 'GST Tax Clubbing' window will appear.

a. Select Period: Here, select that month whose Tax Clubbing entry needs to be generated.

Suppose select 'August 2023'.

b. Avail ITC Prev. Month: ITC means Input Tax Credit. Here, if the user needs to carry forward the Input Tax Credit of the previous month then select 'Yes' else leave this field as blank.

c. Avail ITC Prev. F.Y.: Here, if the user needs to carry forward the Input Tax Credit of the previous Financial year(FY.) then select 'Yes' else leave this field as blank.

d. Post in A/C Books:If the user needs to Post Tax Clubbing in the Account books with report then select 'Yes' otherwise keep it as 'No'.

The user will select other filters as per the requirement.

Click on 'Okay.

- A Marg ERP 9+ alert of 'Tax Clubbing Sheet saved as TAXCLUB_1xls' will appear.

- Click on 'Ok'.

- Now, the user can view the excel sheet of Tax Clubbing entry will get auto open in background.

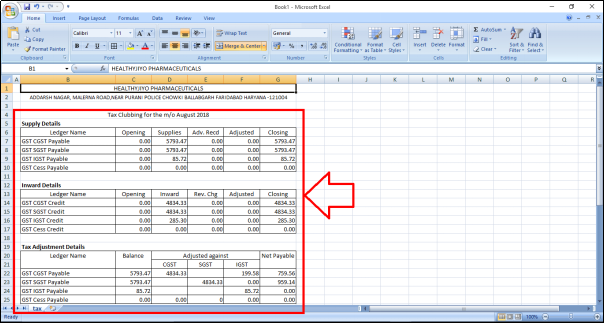

In the excel sheet, the user can view:

a. Supplier Details: Supplier Details indicates the sales part i.e. it displays the outward details in the supplies column of the supply details which has done in a month under CGST, SGST and IGST. Along with it also displays the closing details here.

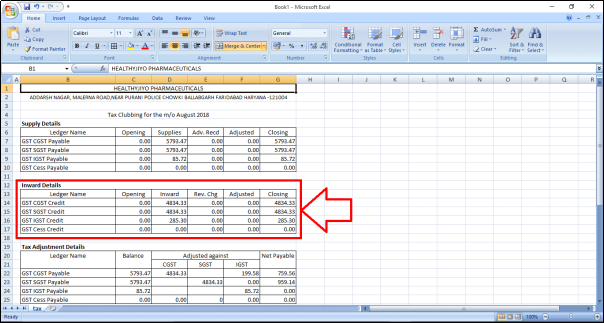

b. Inward Details: Inward Details indicates the purchases done in a month i.e. it displays the details of the purchase has done in a month in the Inward column. Along with it also displays the closing details here.

From here, the software will club Inward and Outward, which can be viewed in Tax Adjustment details.

c. Tax Adjustment Details: Here, in the Balance column it displays the Outward part i.e. Sales part (Supplies) in the Balance column/field and the Inward part i.e. Purchase part (Inward) in the Adjustment against field.

As the Purchase is being deducted from the Sales and the output which is left after the adjustment that amount needs to be further payed to the government.

Note: This whole process is now automatically done by the software which was earlier done manually.

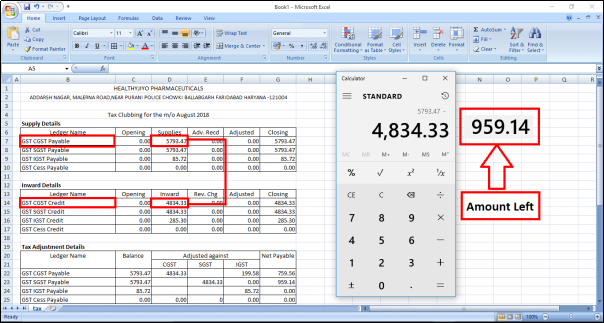

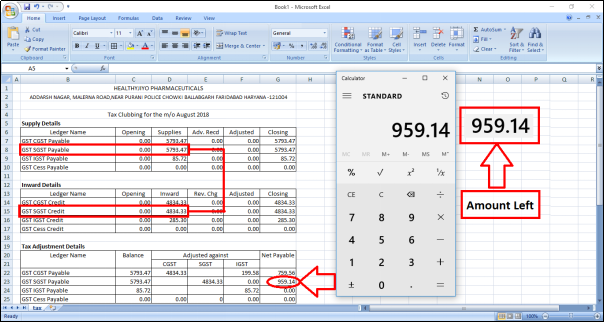

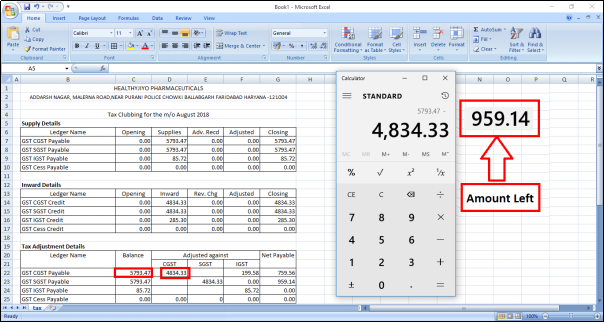

1. CGST Amount Adjustment

For example: The output which is left out from the sales part needs to be deposited with/to the government and the input which is left out from the purchase part (Inward) has to be received from the government.

So, the software has deducted the input from the output i.e. the software has firstly adjusted the CGST Payable with CGST Credit amount.

(E.g. CGST sale done for a month is 5793.47 (CGST Payable). Out of which the software has adjusted the amount of CGST Purchase (Inward) i.e. 4834.33 (CGST Credit). So, now the amount left is Rs. 959.14)

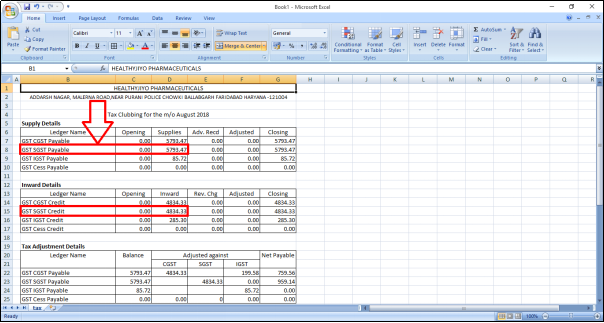

2. SGST Amount Adjustment

Similarly, it will be done in SGST Outward and SGST Inward. SGST Payable is the amount which needs to be paid to the government and SGST Credit is the amount which needs to be received from the government.

- So, the software has adjusted the SGST Payable with SGST Credit amount. And the amount which will be remaining that will be reflected in 'Net Payable' i.e. SGST Payable (Output) is 5793.47. Out of which the software has adjusted the amount of SGST Credit (Inward) i.e. 4834.33. So, now the amount left is Rs. 959.14)

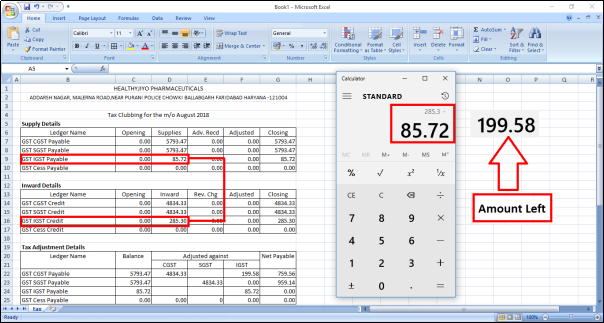

3. IGST Amount Adjustment

Now, IGST Payable of a month is Rs. 85.72 (IGST Sale) and IGST Credit is Rs. 285.30 (IGST Purchase) i.e. IGST Inward is more than IGST Outward of approx. Rs. 200.

As the Sales is being deducted from the Purchase and here also the So, the software has deducted the IGST Credit amount from IGST Payable i.e. the software has adjusted the amount of Rs. 85.72 out of Rs. 285.30. So, now the input left is Rs. 199.58.

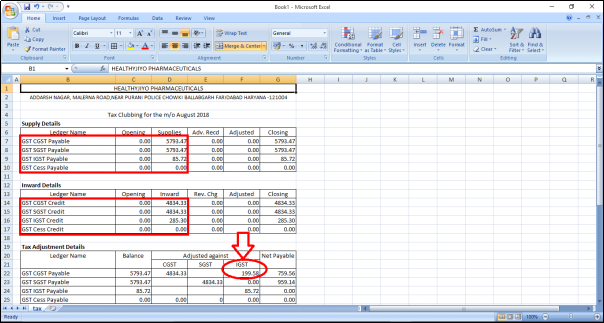

- So, as per the government norms, the amount which is left i.e. Input once the adjustment is being done in IGST Inward and Outward that can be firstly be adjusted in the Central part of the government (CGST Sale) and still if the amount is left after that then that amount can be adjusted with the SGST Outward (SGST Output).

- Similarly, the input which is left after the adjustment of IGST Payable and IGST Credit is approx. Rs. 199.58.

- The software has firstly adjusted this input with CGST Payable (Rs. 959.14) i.e. the amount which was left after the adjustment of CGST Payable and CGST Credit.

- So, the amount which is left after the adjustment of Rs. 199.58 out of Rs. 959.14 is Rs. 759.56(Net Payable) needs to be paid to the government in case of CGST.

- Now, there is no input left which is to be adjusted with SGST Output like it is already been known that firstly IGST Output is adjusted from IGST Input. Then if any input is left then it is adjusted with CGST Output first (Central Sale of Government).

- Then also if any input/amount is left in IGST Inward then it is adjusted with the output which is left in SGST Outward.

- Here, no input is left for the adjustment in SGST. So, Net Payable to the government is Rs. 759.56 of CGST Sale + Rs. 959.14 of SGST Sale and there is no need to pay anything in IGST as it is already been adjusted.

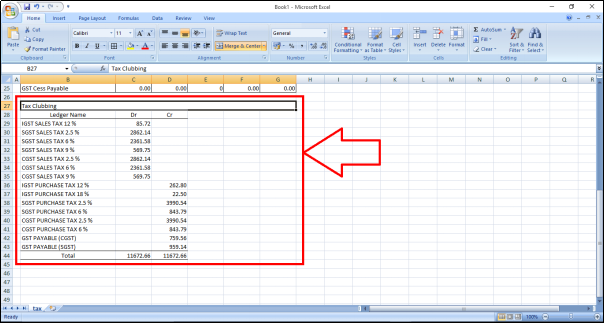

- Now, here the user can view that on which basis the Tax Clubbing is being done i.e. on what type of Tax Slabs IGST Sales & IGST Purchase is being done and along with the amount which is being debited or credited.

- Similarly, the user can also view the Tax Slabs of SGST and CGST along with the debit and credit amount.

In This Page